Downturn deepens + The income you need to buy + No vacancy

Australia’s housing market has taken its sharpest step back in years.

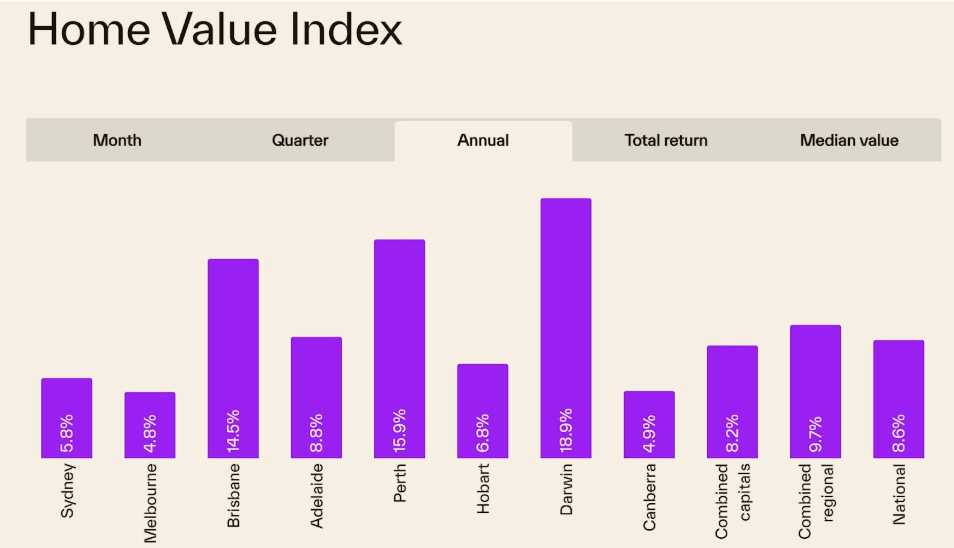

Cotality’s national Home Value Index fell 0.4% between May and June, the largest monthly decline since December 2022.

Sydney led the slide, down 1.2% for the month, while Melbourne fell 1.0% and Canberra dropped 0.6%.

Even the mid-sized capitals are losing steam. Brisbane rose just 0.3% and Perth 0.7%, both a sharp slowdown from the pace of growth recorded earlier in the year.

Cotality research director Tim Lawless said the market is changing rapidly.

“Even before interest rates rose by 75 basis points, we were seeing affordability hurdles weighing on buyer demand. Higher cost-of-living pressures, deeply pessimistic sentiment and a further dampening of demand via property taxation changes announced in the federal budget are all contributing to weaker housing conditions,” he said.

Regional markets are holding up better by comparison, rising 0.3% in June.

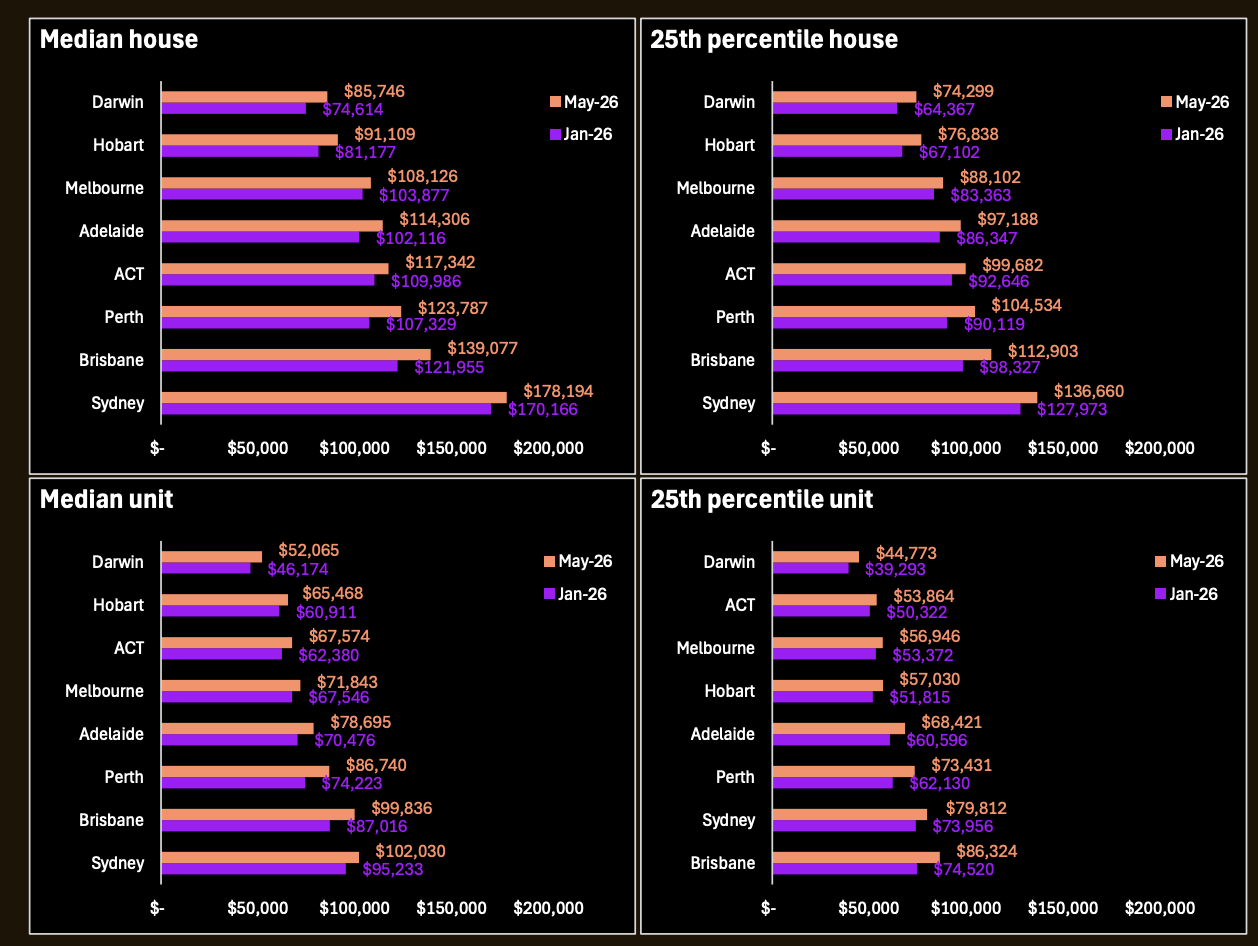

How much do you really need to earn to buy a home?

Three rate rises in 2026 have pushed up more than just monthly repayments. They’ve also lifted the minimum income needed to qualify for a loan in the first place.

New Cotality modelling shows a household now needs to earn at least $178,194 to purchase a median Sydney house, up from $170,166 in January. Brisbane sits at $139,077 and Melbourne at $108,126, the most accessible of the major capitals.

The figures assume a 20% deposit, a 30-year principal and interest loan, borrowing at 6.25%, with a 3 percentage point serviceability buffer applied on top.

For aspiring buyers feeling the squeeze, there are still paths forward. Reducing debt, comparing lenders and broadening the search to include units or regional areas – where income thresholds can be significantly lower – can all help make the numbers work.

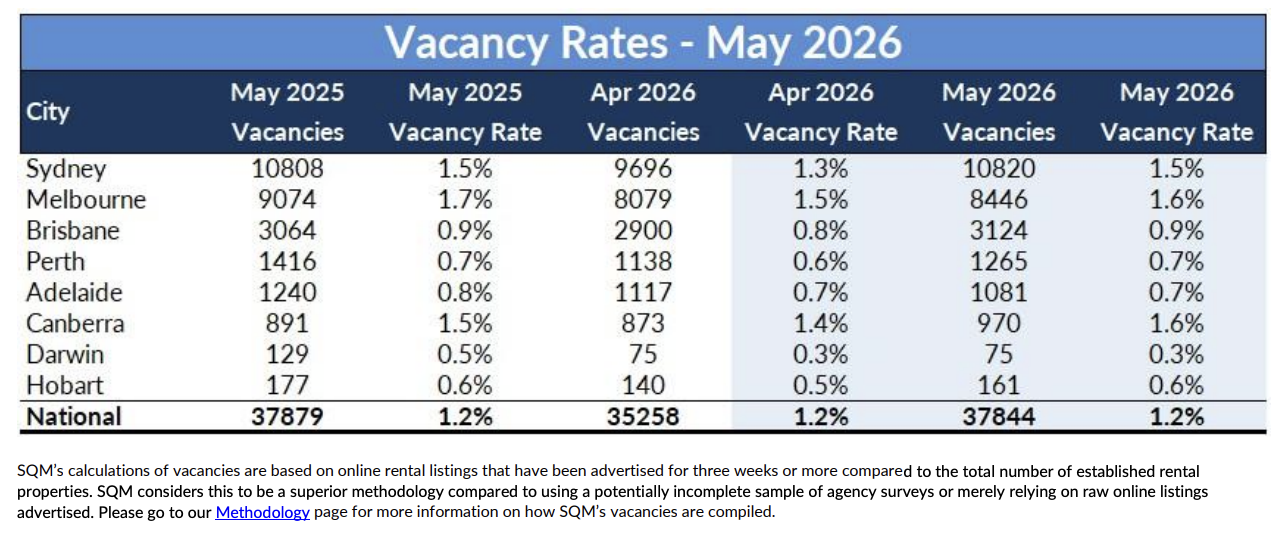

No vacancy: Australia’s rental crisis rolls on

If you’re searching for a rental right now, the numbers explain why it feels so hard.

SQM Research data shows Australia’s national vacancy rate held at just 1.2% in May 2026.

Five capital cities are recording vacancy rates below 1%, led by Darwin at just 0.3%, followed by Perth and Adelaide at 0.7%, Brisbane at 0.9% and Hobart at 0.6%.

To put that in perspective, a balanced rental market typically sits around 3%.

Rents are feeling the pressure too. Annual asking rent growth ranges from 4.5% in Canberra to 14.0% in Darwin, with the national average sitting at 7.8%.

SQM Research managing director Louis Christopher warned that relief is not on the horizon.

“Australia’s rental market remains fundamentally undersupplied. Without a substantial increase in housing construction and rental stock, and/or a meaningful decrease in population growth rates from current levels, affordability pressures are likely to persist through the remainder of 2026 and into 2027.”