Westpac upgrades outlook + Construction gap narrows + Stamp duty outpaces wages

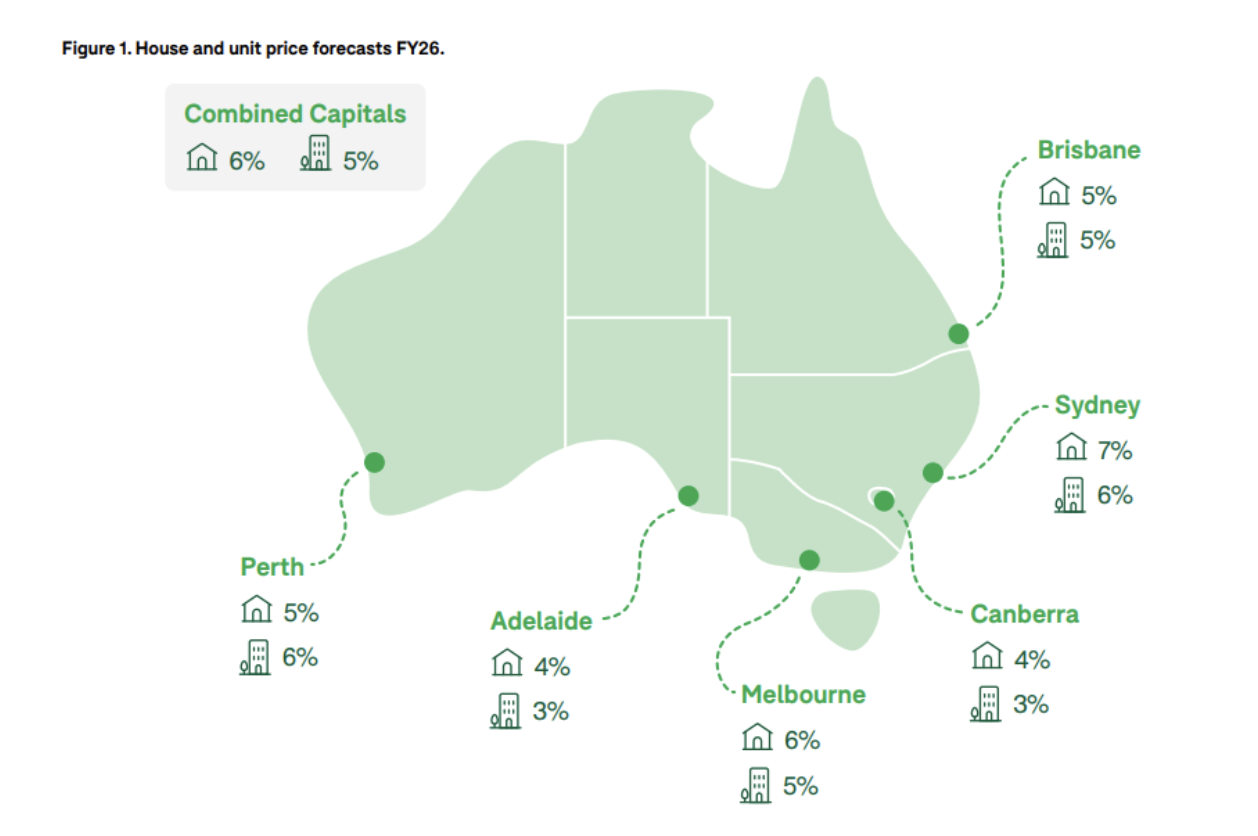

Westpac has updated its property forecast ahead of the spring selling season, and it’s good news for Melbourne homeowners.

Nationally, Westpac expects 6% growth this year and 9% next year. That’s double what it predicted back in May. Melbourne is tipped to lead the charge with 10% growth in 2026, the highest of all capitals.

The bank says interest rate cuts have lifted sentiment, while the number of homes for sale has dropped to just 2.5 months’ worth of supply, well below the usual 3.5 months.

Another key driver is the rise in cash buyers. More retirees are using super to purchase property outright, while growing intergenerational support from the “Bank of Mum and Dad” is helping younger buyers into the market.

Although building approvals are starting to rise – particularly in higher-density housing – Westpac says a meaningful increase in completed homes won’t arrive until late 2026.

In the meantime, demand is likely to keep outpacing supply, giving sellers the advantage.

Buying still cheaper than building, but gap is narrowing

Construction cost inflation is finally slowing – and in some cities, house price growth has caught up. This, in turn, is shifting the buy-vs-build equation.

According to Ray White chief economist Nerida Conisbee, construction costs and house prices are now tracking much closer together. Between 2021 and mid-2025, national construction costs rose 35%, while capital city house prices climbed 32%. That 2.3-point gap is down sharply from 16 points in December 2023.

In Perth and Adelaide, house price growth has actually surpassed construction costs, encouraging new development and strengthening the housing pipeline.

But in Melbourne, the story remains difficult. House prices have risen just 4% over four years, compared to a 25% jump in construction costs. That makes building far less viable, a challenge that’s also playing out in Sydney and Canberra

Stamp duty costs outpace incomes

Today’s buyers face stamp duty costs that are up to three times heavier relative to income than those of 25 years ago, according to Domain.

Domain’s research found that, in Sydney, the stamp duty on a median-priced house was equal to 44.5% of income in 2000. By 2024, it had risen to 119.7%. Melbourne’s share grew from 36.5% to 109.3%, while Brisbane lifted from 19.5% to 66.3%.

Overall, stamp duty has grown 2.7 times faster than wages in Sydney, three times faster in Melbourne and 3.4 times faster in Brisbane.

Domain said that much of the increase is linked to soaring property prices. However, stamp duty thresholds have barely shifted during the same period. This, in turn, has created “bracket creep”, where buyers of even modest homes were paying at rates originally designed for more expensive properties. That structural shift has magnified the burden across the market.

While the burden has grown sharply, there are some relief measures in place. For instance, stamp duty concessions and exemptions are available for eligible first home buyers, although these differ from state to state.